Hungary’s Third Climate Neutrality Progress Report attempts to objectively present various emission trends during 2022, compared to the year 2021 covered in the second report, and to 2020 covered in the first report, thereby informing decision-makers and, in a broader sense, the entire society.

Hungary has a medium performance in international climate policy rankings.

This time, Hungary ranked 49th out of 59 countries in the Climate Change Performance Index, up four places from the previous ranking, ahead of the Czech Republic and Poland in the region. In the Green Futures Index, Hungary was ranked 29th out of 76 in the 2023 report, which uses data from 2020 and 2021 – down 5 places from the previous report – while only 3 EU Member States were ranked ahead.

There has been a significant reduction in GHG emissions, but it is feared that this rate of reduction is not sustainable in the long term, which is what is needed.

In 2022, there was a large drop in GHG emissions. However, this significant reduction has been enhanced by one-off crises in multiple sectors, not by deliberate action only. It, therefore, seems questionable whether the progress made now can be sustained in more favourable economic circumstances, or what new policy instruments could be introduced to help further decarbonisation.

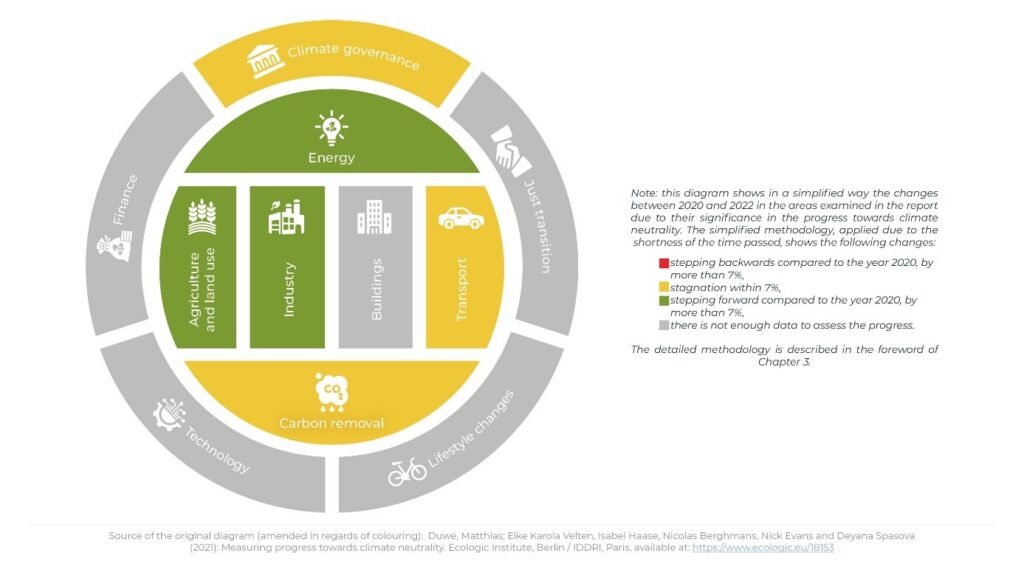

All but one sector is on a stagnating or declining path, with emissions continuing to rise in transport.

GHG emissions in almost all sectors decreased in 2022. The only exception was the transport sector, where the continued growth and aging of the vehicle fleet, the end of COVID restrictions, still partially in place in 2021, and the gasoline price freeze led to significant emissions increases.

Monitoring progress on climate neutrality remains difficult due to data gaps.

For about one-third of the indicators examined, no data were found, making it difficult to assess progress. The situation is further complicated by the fact that for the same indicator, there is data in one year and no data in another. For these reasons, progress in some of the dimensions examined – buildings, finance, technology, lifestyles, and just transition – could not be assessed, one more than the number of sectors that could not be assessed in last year’s report.

Several sectors have moved in relatively good directions, and none have moved significantly in the wrong direction.

Based on the simplified methodology assessment, three sectors have moved in an overall positive direction from 2020 to 2022, namely energy, agriculture and land use, and industry. Another positive aspect is that no sector had to be marked in red. We have observed stagnation in transport, carbon removals, and climate governance. However, the main findings of last year’s report still seem valid, highlighting that while the “hard” (technology-centered) sectors are performing relatively well, it is very difficult to track the evolution of the “soft” (people-centered) sectors due to data gaps.

The full report is accessible below (in Hungarian).